CIPA has released their figures for 2020 production and shipments of cameras and lenses. While it might make for some brutal reading in terms of the bottom line, it was a landmark year for one reason: mirrorless cameras outproduced DSLRs for the first time.

CIPA production and shipment data is a stalwart of the camera industry as it provides some insight into how the sector is developing. These are released on a monthly basis, then wrapped up for the calendar year in the following January. Before looking at the results in more detail, it is worth noting that they show the number of units and value (in Yen) and are presented as items produced and shipped for different global regions. The shipment data includes products that is already in the supply chain (but not necessarily manufactured in 2020) at the shipment price (which is higher than the production cost). So, what did the COVID-19 impact on 2020 look like?

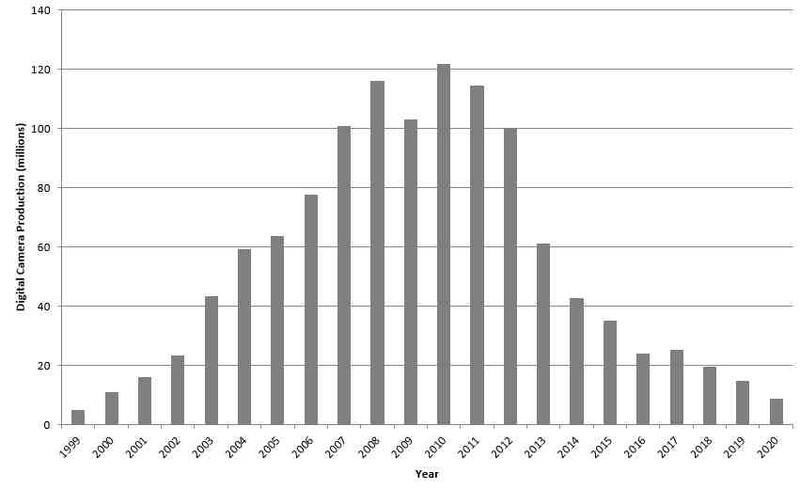

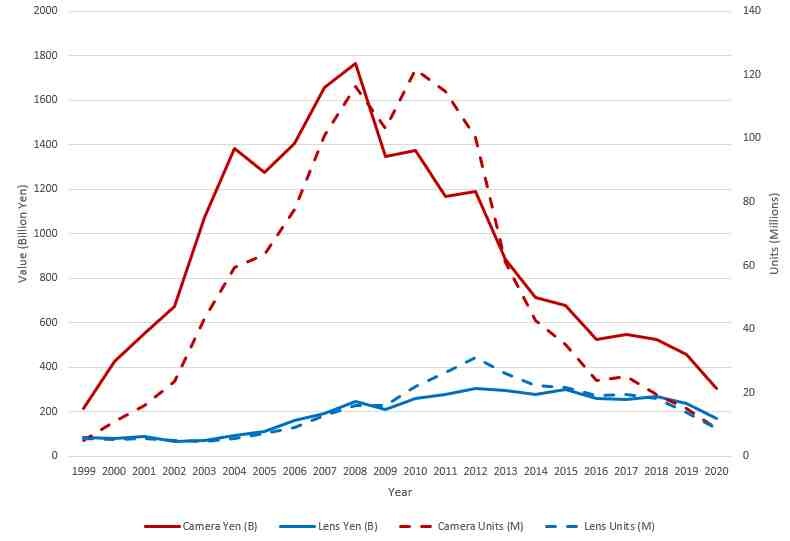

The short answer is that this was a bad year for manufacturers with the total number of cameras produced dropping from 14.8M to 8.7M, the vast majority of those losses coming in the integrated camera line (6.6M to 3.5M), although DSLRs also took a big hit, dropping from 4.4M to 2.4M. Mirrorless cameras weren't spared, dropping from 3.8M to 2.9M. In terms of value, the market reduced from 440B¥ to 303B¥, with the main losers being integrated cameras (reduced by 47B¥) and DSLRs (reduced by 64B¥), although mirrorless cameras also dropped by 26B¥.

CIPA also presents monthly production data, and these imploded from March to June, before going through a recovery with a perhaps better-than-expected Christmas. The total loss in terms of units shipped is principally a result of this.

The Year of the Mirrorless

Perhaps more important than the straight numbers of units shipped is the changing proportions of each camera type. Integrated cameras have declined from 98% of all cameras sold in 2003 to 40% last year; however, they now make up just 20% by value. DSLRs have been in steady decline and now make up just 27% of units and 26% by value. It is mirrorless cameras that are the big story of 2020, now making up 33% of sales, but 54% by value. This is also the first year where more mirrorless units have been produced than DSLRs, although by value mirrorless as a sector was worth more than DSLRs in 2018. That in itself is an important date as it shows just how late Nikon and Canon were at selling seriously into the mirrorless segment.

Looking at unit value, integrated cameras are worth 17B¥ per million units compared to 33B¥ for DSLRs and 56B¥ for mirrorless. The contrast is stark — more mirrorless cameras are being produced at a higher average cost. This is reflected in Canon's recent annual results, which shows better-than-expected performance on the back of strong sales of the R5 and R6.

Changing Regions

Another interesting aspect of this year's CIPA results is the difference between regional shipment data. I've written before about the importance of the Japanese market to domestic producers, with some 25% of integrated camera shipments going there, however that drops to 5% for DSLRs and 11% for mirrorless. In short, different regions of the world are very important, and this isn't the same for each brand. Historically, Europe and then the Americas are the most important in terms of units shipped, followed by China and Asia. What is noticeable is that all regions decreased, except China, which increased its proportion. In short, China is as important as Europe and the Americas to manufacturers, and this growth sector may well feedback to the product design teams. Cameras are unequivocally focused upon the requirements of the different sales demographics. So, will we see a different interplay of features that cater to different requirements?

Lenses

Lens production fared better than camera production, although crucially note that CIPA members include Olympus, Zeiss, Canon, Nikon, Tokina, Tamron, Sigma, Sony, Panasonic, Cosina, Fuji, and Ricoh. That list misses out a large segment of Chinese and South Korean manufacturers, such as Viltrox and Samyang, who are believed to account for about 20% of the market (and growing). There were a total of 8.9M units produced at a cost of 172B¥, down from the 14M units and 236B¥ for 2019. That's a 36% drop in units, compared to 41% for cameras and, as a result, a slight increase in the total share of production value. Note that as many lenses are being produced as cameras sold, and while not to the same total value, they are an important source of income.

The same regional trends hold true, with shipments to China broadly holding steady; however, in this instance, the proportion shipped to Europe and the Americas is still significantly higher at around twice as much each. This obviously reflects lower lens shipments by CIPA members, but whether more lenses are shipped by other manufacturers remains to be seen.

What Does 2021 Hold?

The unabated decline of both integrated cameras and DSLRs will continue, with camera sales being targeted at high-ticket items. Perhaps this is self-evident given the way the market has swung away from the low end. Nikon is perhaps a representative microcosm of this change with a shift of production to low-cost domains, the shuttering of its integrated camera ranges, and the ramping up of mirrorless camera and lens production. At the other end of the spectrum, Pentax has a blinkered approach. In its world, mirrorless cameras do not exist, and the DSLR remains the pinnacle of optical achievement — this is a perfectly plausible strategy. The DSLR market is not going to permanently die away, and maybe the 3% share it holds is all that is needed to keep the brand alive. That leaves Canon and Sony leading the mirrorless charge and arguably benefiting the most from it; they are therefore exciting to watch in terms of product development. The next year will also be an interesting one for Olympus and Fuji. How will Olympus develop under new management given that it still sells a large number of cameras each year? Will we see the continued success of Fuji's X and GFX cameras and lenses, and will they be able to make inroads into Sony and Canon's dominance?

Lead image a composite courtesy of MediaModifier via Pixabay, used under Creative Commons.

Join the Fstoppers community for free

-

Post comments and join in the discussions

-

Browse the site ad-free

-

Share your work and get featured in the community

-

Compete in the photo contests for fun and prizes

1 Comment

I am actually surprised the number of lenses dropped that much considering how many people are now going to mirrorless.