I awoke Friday morning to see a heart-wrenching Facebook post from a friend of mine. She had knocked her camera into a lake.

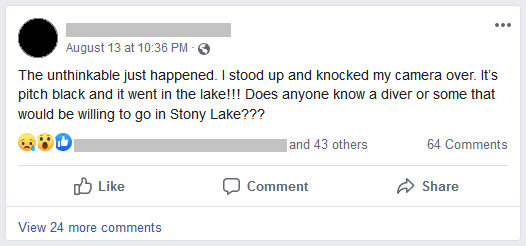

A friend that we'll call "Lisa" was shooting the Perseid meteor shower Thursday night alongside a lake. She was using a Sony a9, Sony 16-35mm G Master lens, L-bracket, Peak Design strap, and a Vanguard carbon fiber tripod, which was firmly planted on a small wooden walkway.

The bugs were horrible that night, and as she stood up to swat them, she heard a splash. Her friend asked if that sound was a fish, to which she replied: "No, that was my camera!" Quite a few f-bombs followed for some time afterward. Not knowing how deep the water was and not being a good swimmer, she elected to not jump in after it. They tried to locate it with a light, but the water was too murky and weedy.

The next morning, when I saw her post, I began to ask her about the location. Having fished there previously, I was familiar with the area. After a few questions, she pointed out on a map where it was. Yep, been there. I knew the water there was only about four feet deep. I told her I would give it a shot, knowing that I would be able to retrieve it if it was still there.

I mounted a hook on an extendable pole I had, grabbed my gear, and headed out. Arriving at the location, I quickly found the marker she had left and set up to video the recovery attempt. I was so excited to see if I could find it that I forgot I had two cameras in my bag. I could have had two angles for the video.

I stuck my hook down in the water and immediately felt what I thought was her camera and tripod. A quick re-orienting of the hook and I snagged the camera rather quickly. I had spent about 70 minutes of travel time and less than five minutes to set up and retrieve the camera.

Here's a short video of the retrieval. Please forgive the framing as I usually don't shoot selfie video with this camera.

The Lesson Learned

Lisa had insurance on her camera gear. She made sure that she had replacement cost coverage and not just depreciated value. A deductible of about $1,100 is much easier to handle than the nearly $7,000 cost for buying new gear. Less than a week after the incident, she had an insurance check for the camera and lens.

She also pointed out that when you get your insurance, you should specify a value that includes sales tax, as that can be quite substantial for gear that is several thousands of dollars. That's certainly something I had not thought about. Insurance isn't the most exciting thing to discuss, but it is essential if you have a lot invested in equipment.

Don't just rely on your homeowner's insurance, as if you use your camera for business, you may require a separate policy. You'll also want to make sure that you have instant coverage, as some policies won't cover your equipment for a set number of days after the policy starts.

Some insurance does not cover trips abroad or only includes a certain number of days. If you travel abroad, make sure to check with your insurance agent.

Don't forget to get coverage for accessories like batteries, memory cards, and other expensive items that may be lost, stolen, or ruined with the camera. While you're at it, you may wish to ask your insurance agent about liability and indemnity coverage if you're a professional.

Do you have camera insurance that you have had to use? Let us know about your experience in the comments!

Join the Fstoppers community for free

-

Post comments and join in the discussions

-

Browse the site ad-free

-

Share your work and get featured in the community

-

Compete in the photo contests for fun and prizes

26 Comments

This is definitely something I haven't been diligent in. Any recommendations I should check out from the audience?

I own Canon 6D, Sony a7iii, Samyang 14, Tamron 24-70, Canon 50 1.8, 35 1.4L II, 85 1.8, Sony 24 1.4, and a bunch of cheaper gear. Not sure what rates I should expect with that amount of gear.

The type of policy you get will depend on whether or not it is used professionally (inland marine policy) or for a hobby (personal articles). I have a personal articles policy through State Farm that insures $3,000 of gear—in my case a drone and a lens—for about $60/year. $3,000 is the minimum coverage. You can figure an extra $20/year per $1,000 of value. IIRC, there is no deductible.

We got the best rates just adding it to our home owner's insurance. And if my camera fell in a lake, you can bet I'd be in that lake within a second, lol.

A friend who is an insurance agent once advised me to be very careful with making claims on home insurance. Because if you have 2 claims (in a 4 year period I believe) you're going to be considered high risk and would be dropped by the insurance carrier. Then I would have to find insurance through a specific high risk home insurer.

Let me say this about that. I put my cameras on the home insurance and began attending workshops. After a few workshops I had two claims. Shooting is always rushed and you are working in the dark every morning and night. Next time my home insurance was up for renewal, Traveler's said they would not renew. I had an excessive amount of claims. I got a new home insurance company and separate camera insurance from Chubb through Rand, which is working with NANPA. You have to be a member of NANPA.

anyone use TCP? A friend filed a claim for $1,500 and he said his insurance premium went up quite a bit (iirc he said $300 a year) after they paid.

Remember that from the company's point of view, insurance is intended to cover catastrophes--business extinction events--not every "oopsie" here and every "aw, shucks" there.

And they have statistics to tell them how often business extinction events should happen to any one business.

So if you've got a comprehensive policy at a good rate with a company known for paying promptly, hold off on claims for a loss you can actually cover with your bank account. Reserve a good insurance policy for the day a gang of thieves break into your studio and completely wipe you out.

Dropped an A9 and 16-35/f4. Two grand of damage (AUD). 400 out of pocket after the insurance pay out.

I had a theft from my locked vehicle of about $8,000 worth of equipment (please don’t lecture me about leaving gear unattended in a vehicle). I filed a claim which was paid. Then they raised my rates. The only claim I had ever made against my home owners insurance in over 30 years. About a year later, we changed insurance companies for a different reason, and they raised our rates for the same theft incident. The rates remained at a higher rate for 10 years. Having said that, the higher rate was still much less in total than the replacement costs.

It took me almost six months to get all the money. Plus they wanted proof of purchase and price for each piece of equipment. My order history at on line vendors was indispensable in this.

I have a rider on my current home owners for such events now. Oh, yeah, and I don’t leave so much as a used tissue in an unattended vehicle now.

Like you, "I have a rider on my current home owners for such events..." because I am not a professional photographer, and I have over $15,000 of gear. It cover whether at home, in a vehicle, out staying out of town.

I was robbed once from my home . . . nearly 25k of gear. I was insured for full value of the gear. The biggest criminals however were the insurance company. They held off, made excuses, delayed, blah, blah, blah . . . until time ran out, almost. 6 months max for a payout. A rep turned up at my door 6 months minus one day, expecting me to fall on my knees and worship them. I was more inclined to take a chainsaw to the son of a bitch. The adjuster also tried many a time to leave him do the shopping for me (complete Sinar kit from an electronics retailer??) . . . biggest scam of all insurance companies. The reason they do that is because they will have a select group of purchasers/vendors who will give them a kick back for purchasing through them. That is standard practice in the insurance business. They only look out for themselves, and are just as much thieves as the people who rob you.

What is the name of the company that rob you?

You are a modern day hero, Mike. No doubt about it.

In just reading the comments, I've learned never to use an a9 near a lake!

It's smart that she has insurance . . . probably one of the first accessories anyone should buy for their gear.

As an aside . . . I had a similar disaster years ago. I was out in a canoe on Lake Champlain which is renowned for having weather that can turn suddenly . . . which it did. I hurriedly paddled to an inlet as the waves grew, finally made it into the shallows, but nonetheless the canoe tipped, giving me and my daypack an unwanted bath. Unfortunately there was a Canon A1 and two lenses in the pack.

Back at camp, fuming, four letter wording non-stop and just generally being thoroughly pissed off, I took off the lens, opened the camera and sat it on a table to dry out (thankfully it was quite windy for hours to come).

Much to my surprise after re-installing a battery the next morning, the damn thing worked . . . perfectly . . . and continued to do so for years after.

Lucky I guess.

Ive got insurance from a company called Ripe insurance here in the UK, i found out that most travel insurance only covers around £1200/1500 for electrical items so wanted something more robust. i think i pay about £120 a year for international cover and it covers the £5500 of gear we carry around when out shooting.

I agree with everybody about insurance but I noticed the tripod she used was a pretty lightweight one. I looked it up to what kind. I have one (Prima Photo) that looks about identical but I would never consider putting a camera the size and weight as a Sony a9 on it. To light and the legs don't spread apart far enough. A stiff breeze would tip it. You can hang some weight from it but no. I won't chance it.

I have a few heavy duty Manfrottos (3050+3063) & (3221W+496) to name a couple of them. I use them with my Canon 70D, 6D and EOS R. I use the little light Prima for my EOS M and Sony action cams.

Had she used a larger tripod with wider leg spread it might have not ended up in the lake.

This is a great point, and you dont have to spend silly Gitzo money to get a great sturdy tripod either, loads of excellent options in the £200/£300 bracket.

Insurance aside (which is super important!), having had my camera take a dip into the Pacific ocean. All times that I'vr shot next to water since, I've had an inflatable armband attached to the tripod. I've seen others use those cables that surfers tie to their boards too! :)

Thank goodness for my USAA Valuable Personal Property policy - it's covered several hundred in repairs with NO deductible - $0 out of pocket. It's so cheap compared to the alternative - you'd be a fool to go without it.

Just filed a 17k claim on my business policy after a rental car break in while in San Fran back in early March. I pay roughly $350 per year in premium, and I got lucky that replacement cost value vs actual cash value is what was in my policy. I had receipts and serial #'s for everything which was crucial for filing the claim as well as real documentation of the incident. Get. Real. Insurance. And do not rely on homeowners or renters policies.

Me too, I’d be in that lake within a second of this happening to me, if for just the attempt at saving the camera or the very least the memory card. However I have two D5 bodies and a D500, maybe the D5 with a weather sealed lens would last a minute I dunno. I do know Sony has admitted the A9 and A9 II are not as robust as the Nikon or Canon flagships. It’s just a fact, not trying to start any arguments and I think Sony makes great stuff! Anyhow the biggest lesson is obviously insurance, I too use State Farm and I pay $230 a year for $15,000 worth of gear. Some of that gear I had to have appraised, but that was easy as a friend of mine owns a photo store. I highly recommend State Farm, my homeowners couldn’t even help me out, ridiculous really. I called around and found most competitors to be double that price. It covers literally everything from accidental like this case, to theft and you name it. It’s the best money I’ve ever spent, however I’ve been extremely blessed, never needed it and never even needed a single repair on Nikon gear in 22 years now. However I keep my NPS membership and insurance for when I will need them.

I have a policy for professional photographers through Hill and Usher. They cover me not only for my gear but also for liability and for failure to deliver, for example if I were to shoot a wedding and have my camera gear and memory cards stolen and so I did not have the wedding photos and got sued. It covers $40,000 worth of gear for $700 a year. The one thing it does not cover is if I teach a class. That requires an additional rider. It also does not cover liability for video shoots which is a separate policy.

I got insurance when I bought a D850 the first year it came out, and replaced all of my older lenses that were not up to snuff. It costs about $300/year. They are a well-respected photo/film insurer in Canada. Like almost all insurance, it is necessary, but optional. I feel better knowing I am covered if something happens when I am out shooting.

Insurance is not necessary ...until your house is broken into, catches fire, your kids knock over your tripod or your camera falls into a lake. There are just too many things that can go wrong in life!

Who in canada do you use for insurance? I have been putting off insuring my gear, but Ive used BCAA for other insurance purposes, so I was thinking of trying that, but would love to hear specialized alternatives!