A camera is only worth what you're willing to pay for it, and the same is true of camera manufacturers. A business is not necessarily the sum of its parts, and its value is reflected in its share price. By this yardstick, Sony is streaking ahead while Nikon is bombing. How do they compare?

Value is a strange concept. If you work for an hour, then your high-end corporate headshot business might charge $500, whereas a startup wedding photographer might charge the same amount for a 12-hour day. Value is an attribute of the buyer and what they perceive the good or service is worth to them. If you find pricing your service difficult, then imagine trying to value your business or a large conglomerate such as Panasonic, yet that is exactly what the stock market tries to do. Once you take your business public and list it on the stock market, you reap the financial reward (and responsibility) of selling a stake. You also become beholden to your shareholders with the sole (corporate) purpose of making a profit, either via dividends or share price increases. And therein lies the rub, your business objective may not entirely align with the profit motive, the latter being how the stock market values your enterprise. You'd like to think that share prices fairly reflect business value, but that rarely seems to be the case, being driven as much by the reaction to current events as corporate insight and understanding. Was Facebook worth $100B when it went public? Or is United Airlines worth $12B, when last year it was close to $30B?

The COVID-19 pandemic is a good example of the complex interplay of stock market investing and shows that uncertainty in life drives uncertainty in markets. For example, the valuations of IT companies have soared during the pandemic, while travel and hospitality have plummeted. The recent announcements of successfully trialed vaccines have caused the opposite effect on business valuations, with the prospect of a return to "normal" for more traditional service-based industries.

Camera Manufacturer Valuation

Valuing camera companies is not too dissimilar requiring an understanding of their assets, along with knowledge of their current and future products coupled with detail on market penetration. Together, these can indicate capital "strength" and so, ultimately, prospects for the future. As I noted at the beginning, a business is not necessarily the sum of its parts. Indeed, this is perhaps the reason for Olympus selling its camera division — as an underperforming business unit, it believed that the future potential was weak and could well have caused it to incur significant costs in the future. By divesting itself of the unit, it may have enhanced the value of the rest of the business even if it's likely that it made no money from the sale itself. Similarly, we see Nikon with an underperforming Imaging Division that is adversely affecting the rest of what is a largely profitable business. It cannot — and does not want to — sell this unit, believing that value will come from returning it to profitability.

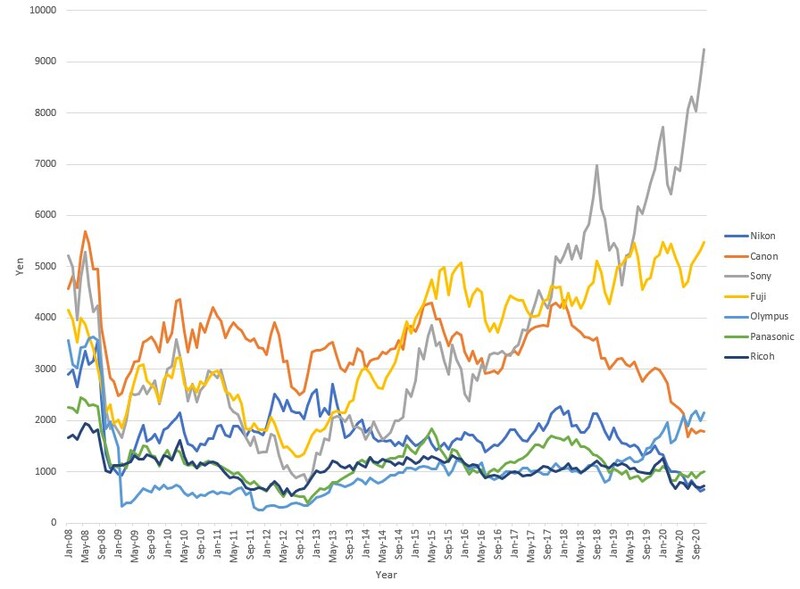

The graph below shows the share price of the seven major Japanese camera manufacturers from 2008 to the present day, although note that it is not adjusted for inflation.

The first obvious thing to note is that these companies have different valuations, although back in 2008, that spread was much smaller (~¥3,000) than it is today (~¥8,000). This reflects the fact that these businesses are different sizes (read a brief summary here) both in terms of sales and employees. Not least, 12 years have elapsed since the start of the graph and a lot has happened over the intervening period. The first change that affected all manufacturers was the 2008 financial crisis where share prices plummeted with Sony perhaps being the most seriously affected (and not long after its acquisition of Minolta). However, camera sales were riding high with income peaking in 2007 and units manufactured in 2010, and this is reflected in the share price bounce-back, except perhaps for Panasonic and particularly Olympus.

Since 2010, there has been a dramatic and consistent implosion of camera sales; however, interestingly, this isn't necessarily reflected in the share price. Of course, this is only a proxy for the market's perceived value, and it's about how good a business is at capturing income. Then came the plunge of 2012, as stock markets rapidly nose-dived because of generally poor business results; this is reflected across the board except for Nikon and Olympus who both remained resilient. However, it is also at this point that we can see the changing fortunes of all these companies to the present day. From that relative high of 2012, Nikon has been in steady decline, barring 2018 which coincided with the release of the Z-system. It is now the least valued business of the seven.

In stark comparison, Fujifilm and Sony have seen significant increases over this period, with Sony's rise inexorable, culminating in explosive gains under COVID-19. Also interestingly, the share prices of Canon, Ricoh, and Panasonic have largely followed the same changes as Nikon; Canon is at an all-time low, while Panasonic and Ricoh are valued at more than Nikon, a rare occurrence. Other than Nikon's poor performance, it is Olympus' steady gains — now valued at more than Canon — that stand out. These have been more marked since the rumors of it selling its camera division first surfaced in 2019 and also under COVID.

Market Insight

Perhaps the most important thing to draw out is that while these are all large corporations, their business interests are diverse. Sony's focus across consumer electronics, manufacturing, and entertainment has seen it develop horizontal and vertical integration while remaining diverse in its income streams. That has been the basis for its success, particularly under COVID, where online entertainment has seen big gains. Fujifilm also diversified from film production and processing in the early 2000s to focus on pharmaceuticals and document management. This has been a highly successful strategy that has allowed it to pursues its own goals for its camera division not solely hindered by profit, which only makes up about 15% of income. In stark contrast, Nikon has remained a solidly optical company that has relied heavily on income from its Imaging Division. It has other income streams, but isn't as diversified as it needs to be, which, coupled with market contraction and the high cost of developing a new mirrorless system, has made the market particularly pessimistic about its future. Canon is not immune from this general outlook even with such a large market share; it is much bigger than Nikon but remains a broadly optical business. Within this context, it's easy to forget about Ricoh and Panasonic, both of whom run successful imaging divisions but have fallen behind their competitors. It remains to be seen whether Panasonic can capitalize on micro four thirds and full frame sales, while Pentax's insistence on remaining DSLR only could well be its death knell. Expect to see change at both these companies.

This brings us back to the notion of diversification — a business needs to play to (or acquire) expertise in areas it wants to profit from, yet at the same time, by monetizing different markets, it should make itself more immune from market volatility. Sony and Fujifilm have demonstrated this well, while Nikon and Canon are suffering from an over-reliance on specific sectors. Olympus has perhaps made the boldest move knowing that its medical instruments and science divisions are where growth lies, believing that their opportunity for profit in camera production has passed. The camera market is now mature with a decreasing number of key players. Innovation is currently in the areas of software and sensor production, particularly in the smartphone sector. Is there an opportunity and, if so, where might it come from?

Lead image courtesy of Mediamodifier via Pixabay, used under Creative Commons.

Join the Fstoppers community for free

-

Post comments and join in the discussions

-

Browse the site ad-free

-

Share your work and get featured in the community

-

Compete in the photo contests for fun and prizes

7 Comments

I remember when this site used to be about actual photography.

https://www.lensculture.com/

If you need a break from fstoppers.

As I’ve said on another article, sites that regularly post photography articles often end up running out of meaningful and useful things to write about. You can tell when articles like this appear.

I thought Olympus was dead.

It's optical division was sold due to lowering sales. Still going for now and the near future.

Ah that is good.

So what happens to it's ambassadors after selling?