Selling cameras is a tough business and it's only getting tougher. The market for digital cameras is contracting at a dizzying rate, so which camera manufacturer is going to fold next?

In recent years we've seen GoPro cancel its drone program, Samsung shift away from ILCs, Casio shut down camera manufacturing, and Lytro pull out of the consumer market. During the Noughties there were a plethora of brands who changed hands or closed their doors, including Pentax, Minolta, Contax, Kodak, Polaroid, HP, and Bronica to name but a few.

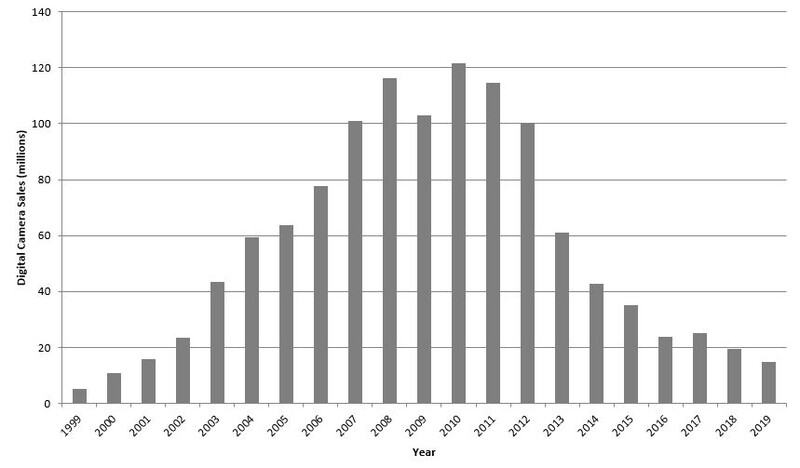

Back then the transition to digital in combination with the mass expansion of compact cameras caught many manufacturers napping or pivoting in the wrong direction. The big winners, at least initially, were the likes of Nikon and Canon who managed to scale production by opening new factories. At their peak, Nikon were selling 30 million units a year — that's more than the entire market shifts today! However what they didn't appreciate was that the seeds of their downfall were sown in the market they had created — namely small cameras, instant photos, and no marginal cost.

Retrospectively, the smartphone can be seen as combining two killer devices — the PC and camera. It's what the general public wanted and, perhaps more than ever, the ability to share photos is possibly the most important feature. As a result phone cameras, and their software, see heavy investment and rapid iteration. Progress is steep. With the likes of multi-billion dollar IT conglomerates such as Apple and Google snapping at their heels, camera manufacturers need to… stay on their toes!

With that in mind, the twenties are perhaps ushering in a second phase of the digital demolition of the camera market. This is something Canon forewarned, anticipating a reduction in the ILC market from what has been a consistent 12M units per year to around 6M. The gradual switch of consumers over to mirrorless will add further complications for lens manufacturers. If the Noughties saw a failure to transition to digital, then the twenties may well be about the inability to pivot to computational processing platforms. There are two challenges facing manufacturers.

Firstly, they are unable to offer significantly better images out of camera and, as a result, can't leverage the lens-sensor benefits to the end user as a matter of course. There needs to be better integration with smartphones — of which there is some progress — and greater investment in in-camera image processing.

Secondly, there's no getting away from the size and convenience of smartphones. A dual-prong approach that also invests in the smartphone sector is needed. You see Leica (with Huawei) and Sony doing this. Samsung saw no benefit in staying in the camera sector, instead focusing it's imaging energies on smartphones. Where are Nikon and Canon in this space? Their silence is deafening.

Current Performance

So what are the prospects of the remaining manufacturers? Sony are probably best placed in the sector ($80B in revenue and 115,000 employees). Their almost exclusive focus upon building a mirrorless ecosystem is now paying dividends after overtaking Nikon to become the second largest manufacturer of digital cameras. In addition, their horizontal and vertical integration across smartphones and sensor manufacture uniquely positions them to offer a degree of convergence not matched by anyone else. The vaulted success of Eye AF demonstrates their commitment to the power of algorithms. Perhaps what is most surprising is that they don't yet offer a smartcamera.

Canon isn't at a small company with sales of $31B and 200,000 employees. It's important to bear in mind that — like all camera manufacturers — cameras aren't Canon's only business (which makes up 25% of revenue) and includes printing and medical imaging. Even so, they remain a dominating force commanding about 40% of all camera sales. What Canon does matters and they aren't going anywhere quickly. That said, their move to mirrorless has been slow at a time when their sales have rapidly contracted. They are now pivoting rapidly, with a firm eye behind them on the fast approaching Sony.

Of the big three, Nikon is in the most worrisome position. It is a camera company through and through and whilst large ($6.5B turnover and 25,000 employees,) with divisions covering medical imaging and precision instruments, what its imaging group does (or fails to do) is important as it accounts for nearly 50% of their income. It's move to mirrorless has been swifter than Canon with it, arguably, matching the offerings from Sony. However Sony is growing largely at the expense of Nikon and so the question is whether the market can sustain three large players.

At the top end, Phase One and Hasselblad specialize in the best possible image quality which increasingly incorporates industrial imaging such as aerial mapping and cultural heritage where the market can bear high margins. Aloof from this group sits Leica, the little red dot generating sales in and of itself. Of the larger active camera manufacturers that leaves Olympus, Ricoh/Pentax, Fuji, and Panasonic. The key questions to ask are: how big is the company, what proportion of earnings does digital imaging comprise (including where video sits), and is this rising or falling.

Ricoh currently employs 98,000 people worldwide and has a turnover of $18B. It is principally a printing/copier business, with the horizontal integration of document management through software-as-a-service (SaaS). Cameras fall in an electrical components division that, as a whole, only accounts for 8% of sales. Ricoh produces a small number of own brand compact cameras — including the desirable GR — having plugged the DSLR gap through the purchase of Pentax. The latter has seen a slow trickle of models with great features and competitive prices, but lagging behind the competition.

Olympus employs over 35,000 people generating a turnover of $7.5B. It has long prided itself on the engineering of its products and championing the MFT sector, however it's the medical instruments (endoscopes) and science divisions that posted the strongest earnings with imaging accounting for 6% of sales. Last year a number of rumors circulated concerning the closure of it's imaging division, however (after a fervent denial) it is business as usual.

Fuji is another big company with 79,000 employees worldwide and a turnover of about $23 billion. Its core business is document management/printing and healthcare. Cameras bring up a distant third place with the imaging section making up only 16% of income —11% from photo imaging and 5% from electronic imaging. In short, digital cameras are small business with Fuji treading a different line to other manufacturers with the dual prong approach of its X-series and medium format cameras.

Panasonic employees 275,000 and with a turnover of $73B is a big company, manufacturing large volumes of consumer electronics focused around display (TV, projector), PCs, DVDs, and cameras, spread across home, avionics, automotive and, industrial markets. Cameras fall within the large Appliances Division which makes up 34% of income, however disaggregating their sales is difficult although in 2018 they were outside the top five manufacturers meaning they had less than 3% market share. That said, they have long promoted the consumer and video oriented micro four thirds format whilst their recent foray in to full frame cameras as part of the L-Mount Alliance marks a new transition.

It's worth remembering that there are a number of manufacturers principally focused on lenses. In addition to their repositioning in the lens market, Sigma's long held niche interest in Foveon sensors has been bolstered by traditional CFA designs since they joined the L-Mount Alliance. Like Sigma, Tokina have transitioned to the pricier end of the market and whilst supporting a range of different mounts might be time consuming, it at least allows them to sell across all brands. Zeiss also occupies this space, but at the very top end of the market where it is able to sell across sectors to other markets that require precision optics. Until 2012 Cosina produced its rangefinder and — having been hitherto nascent — it is set to release the ZX1 shortly which may yet answer the critics of a lack of a computational platform from a traditional manufacturer.

Future Prospects

So where does this leave manufacturers now? The big three will continue to manufacture to the same volume targets for the foreseeable future, with Sony closing in rapidly on Canon. It is Nikon that is in the most precarious position as it is both losing market share and relies heavily on camera sales for its income. Is it conceivable that Nikon could pull out? Yes, but the next five years are critical to its future.

Of the remaining manufacturers, Fuji and Olympus have the largest market shares which leaves Ricoh/Pentax and Panasonic. Panasonic are a very large company and heavily invested in video — so as long as they demonstrate an ROI there is no reason not to continue manufacturing. Perhaps then, Ricoh/Pentax are in the weakest position. Will Ricoh stay in the market? Will they continue to develop new models? Or will they exit, in the way Konica sold Minolta, by putting Pentax (or its entire imaging division) up for sale? One things certain, the camera market is no longer a cash cow and it's reached a tipping point. Who will be left in five years time?

Body image courtesy of OpenIcons via Pixabay, used under Creative Commons and copyright Zeiss.

Join the Fstoppers community for free

-

Post comments and join in the discussions

-

Browse the site ad-free

-

Share your work and get featured in the community

-

Compete in the photo contests for fun and prizes

25 Comments

Pentax

I used to shoot Pentax until I jumped ship to Fujifilm. The K-3 was a good camera, but the X-T2 was just better. It would be a sad day if the world lost Pentax.

Spotmatic F is more iconic t o me then any other camera:)

But when management claims mirrorless is just a wave, it is over.

That’s even worse then Nokia.

I also jumped from Pentax to Fuji. The handling and build quality was way better with Pentax.

I never had a problem with Pentax handling and quality, which I found perfectly fine. For me, it was mirrorless, Fuji film simulations and the lenses which caused me to jump ship. I also really enjoy the dials.

Pentax is part of RICOH

Oly

Since market is shrinking rapidly thus influx of new customers is dwindling. So the companywith large enough loyal customer base would probably be well protected unless they do a lot of unwise things at once...

My guess is many will fold. Canon just announced/released some really strong cameras. Meanwhile, Nikon is still blundering their way through life. I think the two big camera companies will be Canon and Sony.

Not many people seem to know about Canon Tokki. They are a subsidiary of Canon and at one stage owned 100% of the OLED screen market. So while Sony make a lot of money off of the sensors in smartphones, Canon make a ton off of the screens!

I bet all these doom and gloom articles are further hurting sales, average consumer goes online to do research and gets discouraged from buying. If I was just starting out I'd probably just stick to my phone since it seems public opinion, even on camera websites, is that a camera is a waste of money for anyone who isn't a pro.

I conquer.

All those doomsday sayers are really throwing a black shadow over the hobby we all love.

From the tech headed, self centered youtubers, that preach hatred for mammon, to the common man, that have no other goal in life, than to follow said youtubers, and spreed the seed of hate further down the line, on every forum they see.

Every camera manufacturers that don't deliver a new camera every year, that is x time better than the last camera they made, is to those people, doomed to die.

It's so sad.

I hate to say it, but maybe the number of manufacturers needs to shrink in order to keep the rest of the industry alive. Cameras as separate devices are a declining product category thanks to the high quality of smartphone cameras. We are headed for a point where the “amateur” and “snapshot” categories will be gone, leaving only advanced amateurs/prosumers and professionals using dedicated cameras. The downside, of course, is that cameras and accessories for folks like us will go even higher in price. Probably fewer stores caring camera gear too, but we have been seeing that problem for a couple of decades now.

I kept and used my two Nikon D700s for 8 years before I moved to the D810. I've had three D810s for four years and they are reliable and work great and I'll keep them until they die or until A) I get rich enough for at least two D850s, or B) some "full frame" mirrorless system catches my fancy. I'm not the sort of customer these companies want LOL!

I think it'll be Pentax or Olympus that dies - or at least changes ownership - first... although I have a lot of Olympus gear too and I'd hate to see either company die off anytime soon.

Who cares?

Olympus must go. Sensor no bigger than a peanut and lenses that cost the earth.

Haha. You're too funny. :D

The people with above average incomes that wanted better than their Cell Phone camera bought the DSLR however they never learned how to leave the auto setting an use their camera's to it full ability. I saw a women with kids holding a Leica M and snapping pictures of them. I asked her if she was a professional photographer and she said no what makes you think that. I said your holding a professional photographers camera. She said oh my husband bought it for me because it was a good camera. That who was driving sales and they found out that they had to learn something to use the camera so they went back to their cell phones. So now sales are slumping the surge was not sustainable. Before compact digital camera's and cell phones these people were using disposable film camera's and before that the Kodak Instamatic and going way back the Kodak Brownie. The sales were driven by disposable film camera users.

FStoppers is a pay to play website. This is propaganda designed to try to worry people in an industry where the public gets more involved in potential “this and that” more than in any other industry. This isn’t the “noughties” as this article called the nineties (complete lack of actual editing and spell checking, just more proof it’s a garbage piece) and there’s a huge amount of room for camera companies of all sizes. I think the most laughable statements were about Nikon and Leica. The author is clearly an anti fanboy/fanboy himself. Either way, I’d take all of this with a grain of salt. We’re not dealing with small companies here that are actually losing money, and canon and Nikon are both showing losses because they have recently sunk a huge amount of money in to R&D to secure their futures. This speculative “journalism” has to stop. It’s just ridiculous, and companies where you can pay to post an article like fstoppers and petapixel should be looked at for what they are: enquirer style tabloid reporting sites.

Sony and Nikon should be the same logo - LOL!

I think both Ricoh/Pentax and Nikon are in rough waters, but Nikon has probably the biggest chances of getting out of it alive. Their Z line offers good cameras but just like Canon they haven't got the pro stuff out there yet - though at least Canon got the pro glass on their RF mount. Nikon has to make their Z mount work in 2020/21. If they can't they will probably either fold or get bought by their competition. Ricoh or to be more precise Pentax has always been niche and they very much missed the mirrorless train.

Canon is doing very well and so is Sony, Fuji is very much safe thanks to a very loyal fanbase, good glass on a closed mount and good stance with both a full lineup of APS-C cameras from lower budget amateurs to pros and a medium format system that gives Hasselblad quite a competition. Panasonic will never abandon their video business, it's just doing too well. Olympus is king of the MFT market and there is a very loyal fanbase as well. Sigma might just ditch the camera business and stick with producing great glass - which is what they do best.

Who's next? Who knows? I will, however, predict that within five years there will only be four major players in the dslr/mirrorless market. Canon still have 50-60% of the market, Sony will buy Nikon . L have 25-30% of the market and the rest will be shared by Fuji and Panasonic. The medium format guys will play in their own limited market without much difference. Sony makes Nikon's chips and sensors and will eventually just buy them. Panasonic will buy Olympus and continue it's micro 4/3 - full frame attempts.Ricoh will just admit no interest and drop Pentax and their own brands. Leica will continue to cater to high end until it realizes it can't keep up technologically. Third party lens manufacturers will struggle to keep up with microcode changes by the major brands but still offer price competitive products of equal or nearly equal image quality. Exciting time to be in the photo industry.

Leica won’t keep up only if some other tech would replace conventional glass. Breakthroughs would come from mirrorless lagless designs, instant connectivity, better reliability, higher color depth sensor designs. Image quality is already through the roof across the board.

Olympus is gone, pentax is gasping, M4/3 is a dead end, Nikon is hemorrhaging money, there are limited opportunities for tech breakthroughs and smartphones are getting better while prices are skyrocketing. What a

great challenge for the photo industry. Within five years the market will have four vendors, Canon, sony,fuji and panasonic - ignoring those very specialized companies - leica, hasselblad, phase one as examples. Small players will join minolta, miranda,contax,bronica,konica, yashica and others as footnotes in the history of photography.

Whoever said Olympus called it.